All Categories

Featured

Table of Contents

It's crucial to note that your money is not directly invested in the securities market. You can take cash from your IUL anytime, however fees and surrender charges may be connected with doing so. If you need to access the funds in your IUL plan, considering the advantages and disadvantages of a withdrawal or a lending is essential.

Unlike direct financial investments in the stock market, your cash money value is not straight purchased the underlying index. Rather, the insurer utilizes financial tools like alternatives to link your money value growth to the index's efficiency. One of the distinct attributes of IUL is the cap and flooring rates.

What does Indexed Universal Life Insurance cover?

Upon the policyholder's death, the recipients receive the death advantage, which is typically tax-free. The death benefit can be a fixed amount or can consist of the cash money value, depending on the plan's framework. The cash money worth in an IUL policy grows on a tax-deferred basis. This indicates you don't pay taxes on the after-tax resources gains as long as the cash remains in the plan.

Constantly evaluate the policy's details and consult with an insurance policy expert to completely recognize the advantages, restrictions, and expenses. An Indexed Universal Life insurance policy plan (IUL) provides a distinct mix of features that can make it an attractive choice for details people. Right here are some of the key benefits:: One of the most attractive aspects of IUL is the capacity for higher returns contrasted to other types of irreversible life insurance.

What does a basic High Cash Value Iul plan include?

Withdrawing or taking a loan from your plan may decrease its cash worth, survivor benefit, and have tax obligation implications.: For those curious about tradition preparation, IUL can be structured to give a tax-efficient method to pass wide range to the next generation. The fatality benefit can cover inheritance tax, and the money worth can be an extra inheritance.

While Indexed Universal Life Insurance (IUL) provides a series of advantages, it's necessary to consider the potential drawbacks to make an informed decision. Here are some of the key negative aspects: IUL policies are more intricate than conventional term life insurance policy plans or entire life insurance policy plans. Understanding just how the money value is connected to a securities market index and the ramifications of cap and floor prices can be challenging for the average customer.

The premiums cover not just the price of the insurance however additionally administrative charges and the financial investment component, making it a costlier choice. Indexed Universal Life loan options. While the money worth has the potential for development based upon a stock exchange index, that growth is commonly topped. If the index carries out remarkably well in a given year, your gains will be limited to the cap rate defined in your policy

: Including optional attributes or riders can increase the cost.: How the policy is structured, including exactly how the cash money value is designated, can likewise affect the cost.: Different insurance provider have various pricing versions, so searching is wise.: These are charges for taking care of the policy and are typically deducted from the cash value.

Where can I find Indexed Universal Life Growth Strategy?

: The prices can be similar, yet IUL supplies a flooring to assist protect versus market downturns, which variable life insurance coverage policies usually do not. It isn't easy to give a specific price without a specific quote, as rates can vary significantly between insurance suppliers and specific scenarios. It's essential to stabilize the significance of life insurance policy and the requirement for added security it offers with potentially higher costs.

They can help you comprehend the expenses and whether an IUL plan lines up with your financial goals and requirements. Whether Indexed Universal Life Insurance Policy (IUL) is "worth it" is subjective and relies on your monetary objectives, danger resistance, and long-term planning demands. Right here are some indicate take into consideration:: If you're searching for a long-term investment car that supplies a death advantage, IUL can be an excellent alternative.

1 Your policy's money value have to suffice to cover your monthly charges - Tax-advantaged IUL. Indexed universal life insurance as made use of below refers to plans that have not been registered with U.S Securities and Exchange Compensation. 2 Under present government tax rules, you may access your cash money abandonment value by taking government revenue tax-free fundings or withdrawals from a life insurance policy policy that is not a Modified Endowment Contract (MEC) of approximately your basis (total premiums paid) in the policy

How do I compare Iul Calculator plans?

If the policy lapses, is surrendered or comes to be a MEC, the car loan equilibrium at the time would usually be deemed a distribution and therefore taxed under the general policies for distribution of policy money values. This is an extremely basic description of the BrightLife Grow product. For costs and more full information, please contact your financial expert.

While IUL insurance policy might prove important to some, it's crucial to recognize just how it functions before acquiring a plan. There are numerous pros and cons in comparison to various other forms of life insurance. Indexed universal life (IUL) insurance coverage provide better upside prospective, adaptability, and tax-free gains. This type of life insurance policy uses irreversible insurance coverage as long as premiums are paid.

Guaranteed Indexed Universal Life

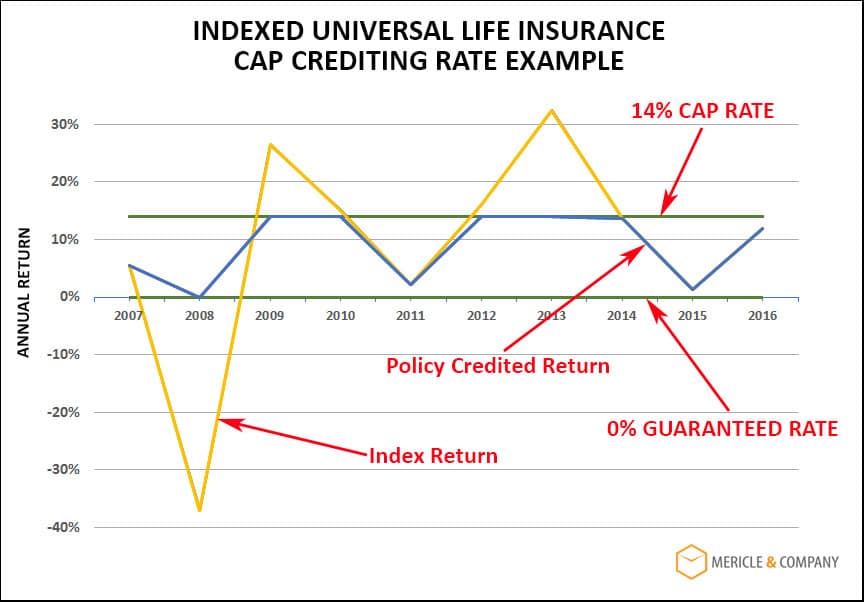

companies by market capitalization. As the index relocates up or down, so does the rate of return on the cash value element of your policy. The insurance business that provides the policy may provide a minimal surefire rate of return. There may likewise be a top limit or rate cap on returns.

Economists often recommend living insurance coverage that's equivalent to 10 to 15 times your annual earnings. There are numerous downsides related to IUL insurance coverage that movie critics are fast to point out. For example, a person who establishes the plan over a time when the market is executing badly could wind up with high costs payments that do not contribute whatsoever to the cash worth. Indexed Universal Life premium options.

In addition to that, bear in mind the complying with other factors to consider: Insurer can establish engagement prices for how much of the index return you obtain each year. Allow's claim the plan has a 70% involvement price. If the index grows by 10%, your cash money value return would certainly be just 7% (10% x 70%).

Is Iul Vs Term Life worth it?

Furthermore, returns on equity indexes are typically covered at an optimum amount. A policy might say your maximum return is 10% annually, regardless of exactly how well the index does. These constraints can restrict the real rate of return that's credited towards your account annually, no matter just how well the plan's underlying index carries out.

It's essential to consider your individual danger tolerance and financial investment goals to make sure that either one aligns with your total strategy. Whole life insurance coverage plans commonly include an ensured rate of interest price with foreseeable superior amounts throughout the life of the plan. IUL plans, on the other hand, deal returns based upon an index and have variable costs with time.

{kind=link}

Table of Contents

Latest Posts

Iul Vs Roth Ira

Maximum Funded Indexed Universal Life

Insurance Company Index

More

Latest Posts

Iul Vs Roth Ira

Maximum Funded Indexed Universal Life

Insurance Company Index